Paramount offers film JV sale to ease Warner deal approval in EU

Paramount offers film JV sale to ease Warner deal approval in EU  Shashi Shekhar Vempati gets Padma Shri honour

Shashi Shekhar Vempati gets Padma Shri honour  TV channels steady, DTH shrinks; telecom, b’band subs up Jan-Mar quarter

TV channels steady, DTH shrinks; telecom, b’band subs up Jan-Mar quarter  MIFF premieres animated series on India’s women trailblazers

MIFF premieres animated series on India’s women trailblazers  Network18 reaches 250mn TV viewers, crosses 65bn social video views: Akash Ambani

Network18 reaches 250mn TV viewers, crosses 65bn social video views: Akash Ambani  ‘Bodhi Tree Multimedia Ltd’ secures Assam digital platform deal

‘Bodhi Tree Multimedia Ltd’ secures Assam digital platform deal  Karisma Kapoor birthday special on ‘India’s Best Dancer 5’

Karisma Kapoor birthday special on ‘India’s Best Dancer 5’  News18 Marathi hosts ‘Krishi Parishad 2026′ on modern farming

News18 Marathi hosts ‘Krishi Parishad 2026′ on modern farming  OS Studios appoints Ishaan Arya as India country manager

OS Studios appoints Ishaan Arya as India country manager  ‘Eetha’ teaser out: Shraddha Kapoor’s powerful transformation

‘Eetha’ teaser out: Shraddha Kapoor’s powerful transformation

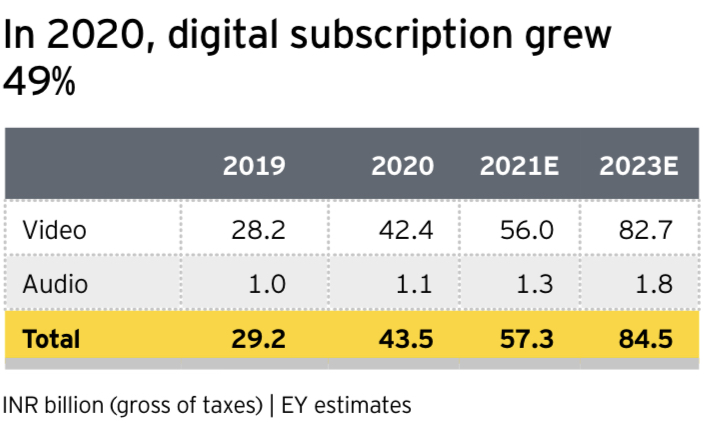

Overall digital subscription and video subscriptions revenue in 2020 registered growth of 49 per cent and 50 per cent, respectively as fresh TV programmes failed to be introduced and premium content —originals and sports — went behind a paywall, particularly during the pandemic, according to a new report.

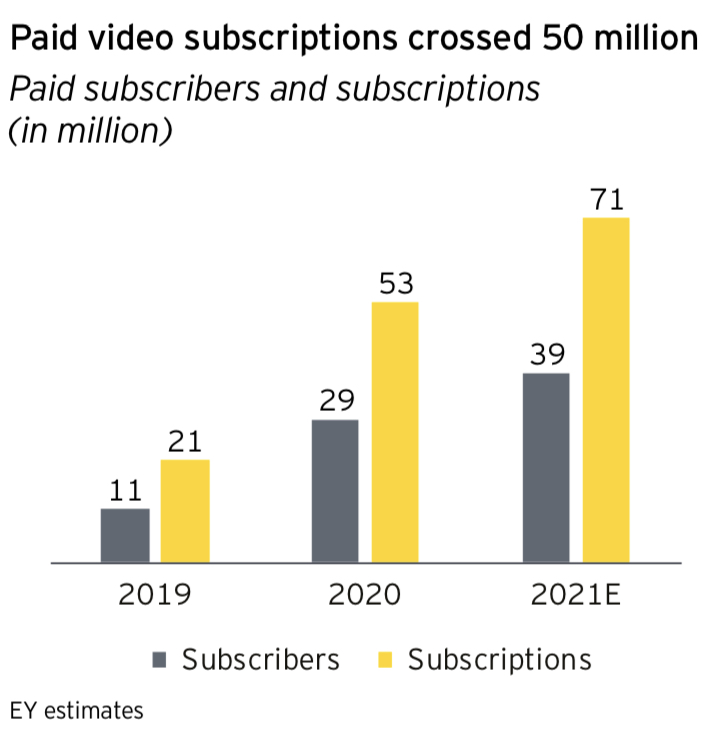

Paid video subscriptions crossed 50 million for the first time, while audio subscription grew comparatively slower at 15% in 2020 as several free products were available that reduced the need to subscribe.

The percentage of paying subscribers to total OTT consumers remained less than 10% and 1% for video and audio, respectively, according to Ficci-E&Y Indian media and entertainment 2020 report.

The report stated 29 million subscribers paid for 53 million OTT video subscriptions in 2020 (not counting subscriptions bundled along with data plans) where the key drivers for growth included Hotstar putting the IPL behind a paywall, release of direct to digital movies during the pandemic and lack of fresh content on television for four months.

OTT players spent upwards of INR 10.2 billion on creating around 1,200 hours of original content across 220 titles in 2020, excluding acquired movie rights and sports.

However, this content spent by streamers is lower than INR 14 billion in 2019 for around 385 titles due to stoppage of shoots during the pandemic for several months. For example, Netflix invested INR 30 billion in content in India across 2019 and 2020 and has announced over 60 titles in India and several other launches in 2020 alone, making India one of its largest content production hubs worldwide.

Disney+ Hotstar claimed 26 million paid subscribers by the end of November 2020 on the back of the IPL going behind a paywall.

OTT players are expected to increase spends on original content to around INR 19.2 billion in 2021 (a 17% growth over 2019) and further increase their total investment in content (including sports) during 2021-25 to INR 300 billion.

Around 500 original titles are expected to be released in 2021 across platforms, but interestingly language streamers proliferated in 2020 with the entry of language OTT products like aha (Telugu), Koode (Malayalam) and City Shor TV (Gujarati).

“Language OTT platforms enable a deeper understanding of audiences and can provide wider offerings than just entertainment content, including religion, news and games,” the report said.

Some of the other trends highlighted for the digital sector in the report include the following:

► 284 million consumers consumed video content through data bundles.

► Telcos and aggregators provided premium OTT subscriptions bundled along with data and/or devices for as little as INR 150 per month.

► Up to 85% of viewership volumes of certain OTT platforms were generated by telcos.

► The amount telcos paid for content was around INR 7 billion in 2020 and is expected to grow.

► It is expected around 400 million consumers to consume content via telco and aggregator bundles by 2025 across a mix of minimum guarantee and per-stream deals

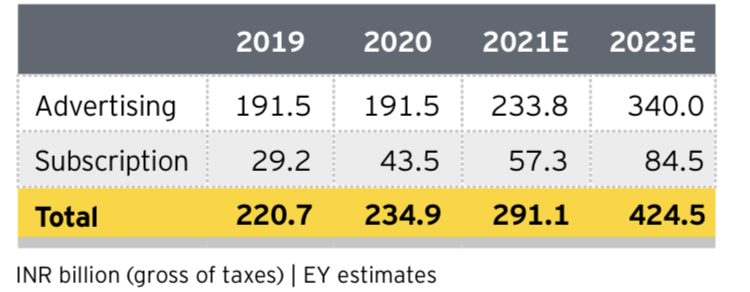

► Digital advertising remained at INR 191.5 billion in 2020 while becoming the second largest advertising segment after television.

► While certain sectors like Travel showed marked decline, sectors like M&E, Auto, BFSI, Durables and Telecom increased spends as they implemented or widened digital sales channels during the pandemic.

► SME and long tail advertisers spent an estimated INR 90.6 billion, primarily on performance advertising on Google, Facebook and e-commerce platforms.

► Of the total, share of ad revenues generated by e-commerce platforms increased to INR 35 billion, crossing 12% of total digital advertising.

► Total advertising including SME & long tail grew by 1% in 2020.

► The top categories contributed 78% of total digital ad spends.

► Internet penetration increased 11% to reach 795 million, of which 747 million had broadband access.

► 45% of India’s population over 15 years of age had access to a smartphone by December 2020.

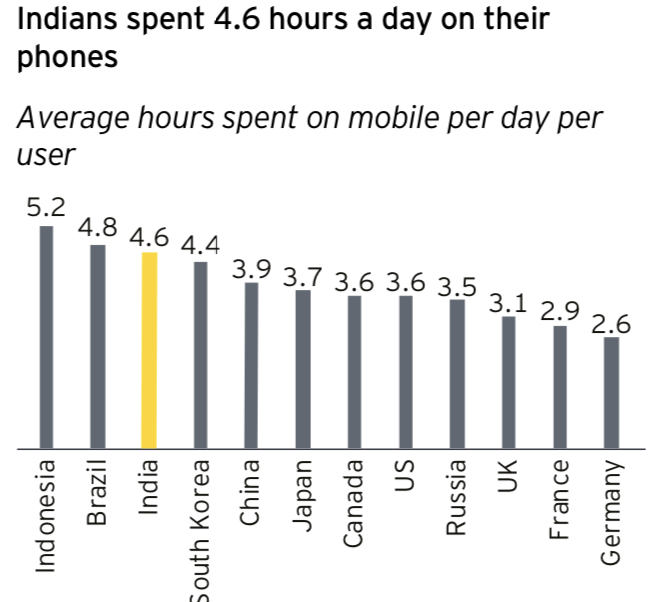

► Indians spent 4.6 hours a day on their phones, increased data consumption by 15% over 2019 and aggregated 450 million online entertainment consumers in 2020.

► Digital subscription grew by almost 50% as the pandemic and the consequent lockdown reduced fresh content on television, online sports went behind a paywall and the pandemic forced much of the population for longer periods indoors.

► Subscription revenue, which was 3.3% of the segment in 2017, had increased to 19% by 2020.

►Internet subscriptions grew 11% between December 2019 and December 2020; yet, just 68% of telecom subscriptions accessed the internet.

►Smartphone users reached 448 million in 2020.

► 94% of those accessing the internet used broadband.

► While narrow band subscriptions fell 16%, broadband subscriptions grew 13% during 2020.

► Urban internet subscriptions grew 7% while rural internet subscriptions grew significantly faster at 17%.

► Smartphone subscriptions increased from 620 million in 2019 to 760 million in 2020, indicating a growth from 1.6 to 1.7 subscriptions per smartphone.

► India remained the second largest market by app downloads in 2020, behind China.

► Indians downloaded almost 24.3 billion apps in 2020, a growth of over 20% over 2019.

► In terms of revenue, India lagged many smaller markets.

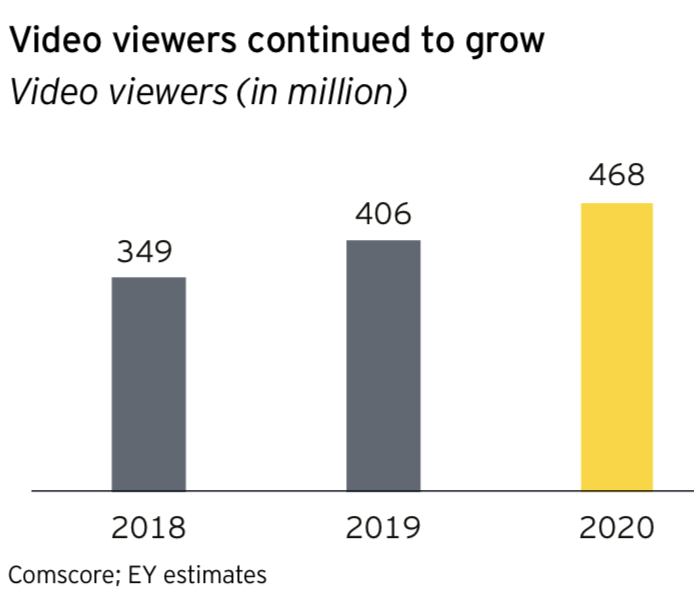

► Video viewers increased 15% to reach 468 million, which is around 96% of smartphone owners.

► Video viewers are expected to grow to 650 million by 2023.

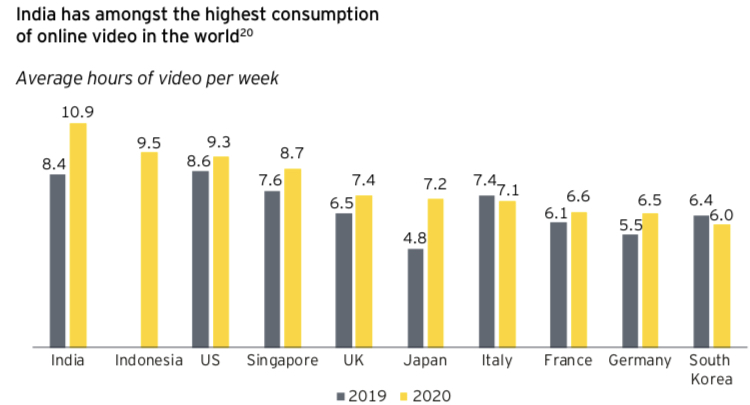

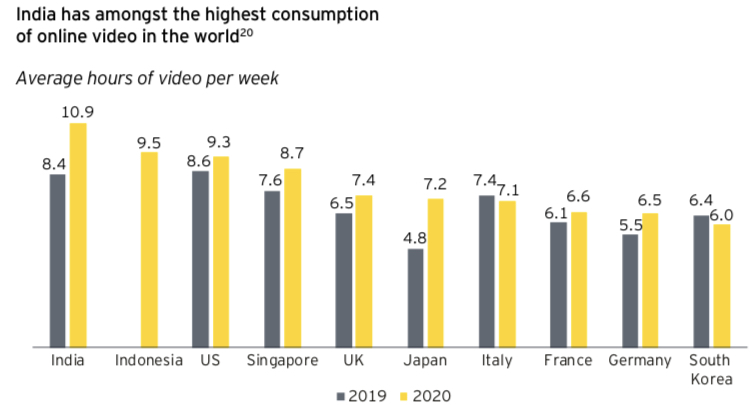

► Viewers in India watch the most online video each week at an average of 10 hours 54 minutes, an increase of 30% from 2019.

► Around 200 million people streamed music online in 2020 on a monthly basis, though around half of those were regular listeners21

► As per a 2020 study by Kantar and VTION, India’s audio streaming market is dominated by Gaana (30% share), followed by JioSaavn (24%), Wynk Music (15%), Spotify (15%), Google Play Music (10%), and others (7%).

► Apart from the rise of regional language music, which contributed 39% of all streams, up from 33% in 2019, the lockdown also saw growth in specific playlists such as cleaning, home workouts, kids’ content and cooking.

► Online news platforms have increased their reach in 2020 as circulation of physical newspapers faltered. ► Dailyhunt was the only news aggregator amongst the top news platforms.

The report did some crystal-gazing and some of the highlights of future trends are the following:

► The report expects digital subscriptions to grow at a CAGR of 25% till 2023; the digital segment is expected to grow to INR 424.5 billion by 2023 at a 22% CAGR.

► The segment became the second largest segment in 2020, overtaking print, and we expect it to continue to reduce the gap with television as digital infrastructure (screens, broadband connections, e-commerce, digital payments, etc.) continue to grow

► Digital advertising will outpace all other media and digital advertising will grow at a 21% CAGR, to equal television advertising by 2024 or 2025.

► Advertising on E-commerce platforms will reach INR10 billion by 2025 as e-commerce players like Amazon, Flipkart, Jio Platforms, Tata, Zomato and others growth their reach and active users.

► The CPT will emerge as the common metric for cross-media measurement and the M&E sector will need to provide models to measure it.

► The metrics that matter will change from MAU to DAU and from audience numbers to engagement, loyalty and time spent, leading to platforms focusing on segmented audiences and community ownership.

► More advertisers will implement ad fraud management solutions and validate ad spend efficiency as digital becomes a larger portion of their media mix.

► Digital subscription will achieve scale and revenues will grow at 25% CAGR as paid subscriptions double to over 100 million by 2023.

► Newspaper digital products will increasingly go behind paywalls and it is expected news and related products to generate subscription revenues of INR 4 billion by 2023.

► Subscription will be driven by genres like women, audiences aged 50 years or above and non-metro audiences.

► The sharing economy will not pass by the digital media space – we could see group subscription products across families, friends, neighbors, colleges and corporates come into being.

► E-commerce apps will provide a significant opportunity to license news, library and interactive content on to their platforms to increase time spent and visitations.

► Demand for original content will double by 2023 from 2019 levels to over 3,000 hours per year.

► Curated short video platforms will garner 25% of total time spent on online video viewing by 2023.

► Share of regional language consumption on OTT platforms will cross 50% of total time spent by 2025, easing past Hindi at 45% .

► Sports will play an increasingly important role in growing subscription revenues and this could lead to a growth in valuation of digital media rights.

► The proposed content code will require implementation of processes for content curation, checks and monitoring controls

► Content costs will continue to increase as the overall quality benchmark rises to address the needs of a more aware audience, particularly across regional markets.

► As the number of connected smart televisions grows to approximately 40 to 50 million by 2025, 30% of content consumed on such screens will not be broadcast content, but gaming, social media, short video and content products specially created for this audience by television, print and radio brands.

► Around 400 million subscribers will consume content bundled by telcos or aggregated by ISPs, cable and DTH companies, as part of their mandate to assimilate OTT content with pure television content to protect and/or grow their subscriber base.

► As screen ratio tends to shift towards 3 small screens against 1 large screen, the type of content being produced will change to reflect the opportunity that 750 million small screens will provide viz, an increase in niche, interactive and personal content.

► Business models will prioritize customer lifetime value and they will be driven by the size and stickiness of the addressable D2C audience base, with a loyal paying subscriber base attracting the highest valuations.

► Products will either focus on mass advertising models or, in many cases, smaller but more cohesive communities, monetizable across a range of transactions apart from content

► Business models of aggregators would need to be realigned if regulation around payment for aggregated news comes into being and if audio streaming subscription revenues fail to grow

► Investors will have little patience for business models with negative customer lifetime values over the medium term and will look to leverage consolidation and partnership opportunities to achieve marketing and operating efficiencies.