DD’s ‘Ramayan’-fame Sagar Pictures forays into global studio biz

DD’s ‘Ramayan’-fame Sagar Pictures forays into global studio biz  JioStar announces six ‘Bigg Boss’ editions from September

JioStar announces six ‘Bigg Boss’ editions from September  MIB seeks feedback on digital news rules

MIB seeks feedback on digital news rules  Maharashtra, Centre step up preparations for WAVES 2027

Maharashtra, Centre step up preparations for WAVES 2027  ‘Blade Runner 2099’ to debut on Prime Video Nov 25

‘Blade Runner 2099’ to debut on Prime Video Nov 25  Prime Video to premiere ‘LOTR: Rings of Power’ S3 Nov 11

Prime Video to premiere ‘LOTR: Rings of Power’ S3 Nov 11  Netflix announces ‘Happy Old Year’ series adaptation

Netflix announces ‘Happy Old Year’ series adaptation  Cooper Koch, Sarah Bolger join cast of ‘Fog City’

Cooper Koch, Sarah Bolger join cast of ‘Fog City’  Meta upgrades AI assistant with task automation

Meta upgrades AI assistant with task automation

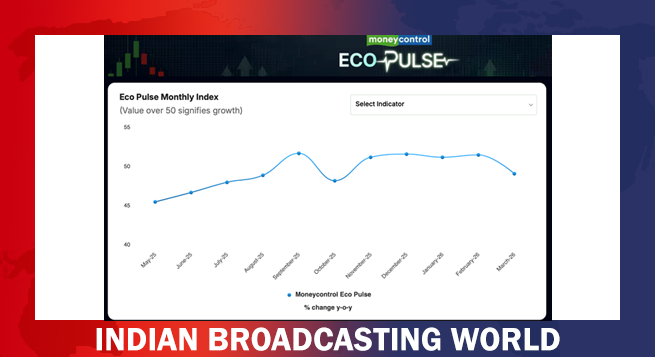

India’s economic activity saw a noticeable slowdown in March, with the Moneycontrol Eco Pulse Index slipping to 49 from 51.4 in February, indicating a contraction in overall momentum. The decline reflects the early impact of geopolitical tensions in West Asia, which have begun to weigh on manufacturing output, infrastructure activity, and external trade.

According to a Moneycontrol press release, the index—based on 38 high-frequency indicators spanning consumption, manufacturing, labour, trade, and financial activity—provides an early snapshot of the economy ahead of official GDP data. A reading below 50 signals contraction, suggesting that while domestic demand remains somewhat resilient, external shocks have started to drag growth lower.

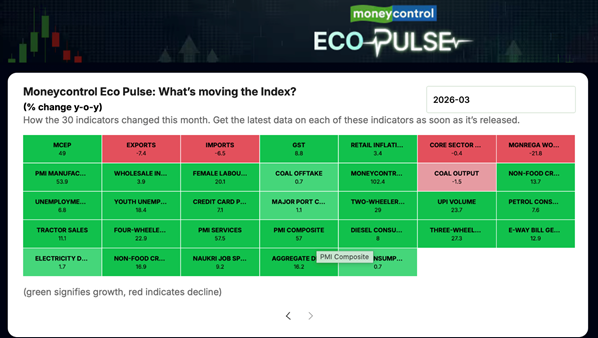

The sharpest pressure came from manufacturing and infrastructure-linked sectors. The HSBC India Manufacturing PMI fell to a 45-month low of 53.9 in March, down from 56.9 in February, pointing to slower factory activity amid rising input costs and supply chain disruptions. Core sector output also slipped into contraction, shrinking 0.4 percent after expanding 2.8 percent the previous month, with sectors such as coal, electricity, and refinery products showing weaker momentum.

Trade indicators further underscored the slowdown. Merchandise exports declined 7.4 percent year-on-year in March, extending the drop seen in February, while imports fell 6.5 percent, reflecting softer global demand and increasing uncertainty. Electricity demand growth, though still positive at 1.7 percent, remained subdued compared to earlier months, indicating softer industrial consumption.

Despite these pressures, consumption trends offered some support to the economy. Vehicle sales remained strong, with four-wheeler sales rising 22.9 percent and two-wheeler sales growing 29 percent, signalling steady retail demand. Fuel consumption also held up, with petrol demand increasing 7.6 percent, suggesting continued mobility and logistics activity. Digital transactions, particularly through UPI, remained robust during the month.

The labour market presented a mixed picture. Urban unemployment edged up slightly to 6.8 percent from 6.6 percent, while the Naukri Job Speak Index moderated to 9.2 percent, indicating softer hiring sentiment. Female labour force participation also saw a marginal dip, reflecting ongoing challenges in employment dynamics.

Inflationary pressures added another layer of concern. Wholesale inflation rose to 3.9 percent in March from 2.1 percent in February, largely driven by higher commodity and fuel prices linked to the West Asia conflict. The data highlights how quickly global disruptions can transmit into domestic conditions through rising crude prices, freight costs, and supply bottlenecks.

Global agencies have already begun adjusting their outlooks. Moody’s Ratings has lowered India’s growth forecast to 6 percent, citing the impact of the oil shock, while the World Bank and International Monetary Fund remain relatively optimistic, projecting growth of 6.6 percent and 6.5 percent respectively for FY27.

While the March reading signals a loss of momentum, continued strength in domestic consumption and digital activity could help cushion the slowdown if external conditions stabilise. Much will depend on how global trade flows and commodity prices evolve in the coming months, as India navigates a complex mix of internal resilience and external headwinds.